The coffee market stabilised slightly in February, but prices remain at very low levels. A lack of news regarding fundamentals with expectations of a large 2016/17 crop in Brazil have kept prices from maintaining any significant rally. Inventories in importing countries have been well replenished, giving a buffer against any immediate supply concerns. Finally, our initial estimate of world consumption in 2015 suggests a steady increase to 152.1 million bags, up from 150.3 million in 2014.

The monthly average of the ICO composite indicator settled 0.8% higher in February on 111.75 cents/lb, but daily prices finished the month weakly on 110.07 cents. The three Arabica group indicators all averaged higher compared to last month, but Robustas fell for the fourth consecutive month to their lowest level since May 2010.

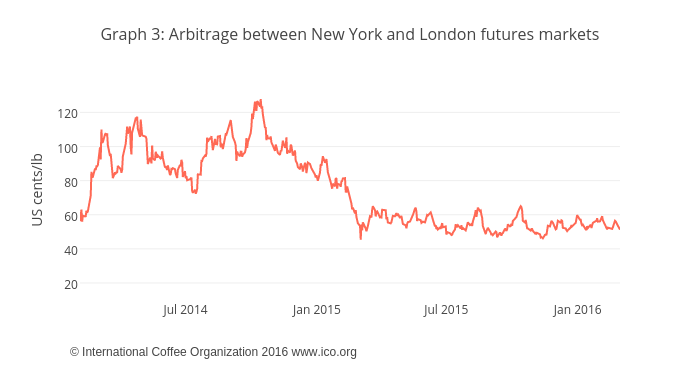

The arbitrage between New York and London was mostly unchanged compared to January, but the differentials between the three Arabica groups and the Robusta indicator all increased. Furthermore, the differentials between the Arabica groups and the New York futures price have all been increasing recently, suggesting a potential for price increases that has not yet been observed in the futures markets.

Total exports in January 2016 came to 9 million bags, just 0.8% less than January 2015, although total exports for the first four months of the coffee year (October to January) are up 1.7% on 35.9 million bags. Exports from Brazil have started to slow, with January shipments down 10.2% compared to last year, suggesting that stockpiles might finally be wearing thin, although this is still a significant volume of coffee. Exports from Vietnam, on the other hand, are estimated up by 10.1% to 2.3 million bags. Colombia continues to export higher volumes, with production levels for the first third of the crop year already on 5.3 million bags.

Looking ahead, there are increasing reports that dry weather resulting from El Niño could potentially affect production in Vietnam, Indonesia and Colombia over the next few months, although any deficit could likely be covered by the increase in output expected from Brazil and Central America.

Furthermore, inventories in importing countries have been replenished, with the European Coffee Federation reporting green coffee stocks of 11.9 million bags in December 2015, up from 11.5 million the previous year. The US Green Coffee Association also reported an increase from 5.5 million bags to 5.8 million, which gives roasters a decent buffer against any short-term supply concerns.

Our initial estimate of world coffee consumption in calendar year 2015 comes to 152.1 million bags, up from 150.3 million in 2014, but a slightly more modest increase than in recent years. The average annual growth rate over the last four years remains at a healthy 2%. Demand in the world’s largest consumer, the European Union, has stagnated slightly at an estimated 42 million bags, averaging growth of 0.8% per year since 2012, but the USA continues to show an increased appetite for coffee, increasing by an average rate of 3.2% to an estimated 24.4 million bags. Japan also continues to expand, averaging 2.4% growth to 7.6 million bags. As a result, total consumption in all importing countries is estimated at 104.9 million bags.

Exporting countries have generally shown more dynamic demand patterns in recent years, and this trend has continued in 2015. Consumption growth in Brazil has slowed to an average of 0.5%, but remains high on 20.5 million bags. Much of the recent growth has come from Asia, with Indonesia, the Philippines, India and Thailand all growing at between 4.5 and 9%. Total consumption in exporting countries is therefore estimated at 47.3 million bags, at an average annual growth rate of 2.3% over the last four years.

(Source: ICO)